![]()

8006 Practice Exam Tests Latest Updated on Sep-2021

Pass 8006 Exam in First Attempt Guaranteed Dumps!

NEW QUESTION 56

What is the day count convention used for US government bonds?

- A. Actual/Actual

- B. Actual/360

- C. Actual/365

- D. 30/360

Answer: A

Explanation:

Explanation

The day count convention used for US treasury bonds is Act/Act. The other choices are incorrect.

NEW QUESTION 57

If the zero coupon spot rate for 3 years is 5% and the same rate for 2 years is 4%, what is the forward rate from year 2 to year 3?

- A. 1%

- B. 7.03%

- C. 2.03%

- D. 4.5%

Answer: B

Explanation:

Explanation

The forward rate from year 2 to year 3 in this case can be derived as =(1.05^3/1.04^2) - 1, or 7.03%. All other answers are incorrect.

NEW QUESTION 58

Which of the following assumptions underlie the 'square root of time' rule used for computing volatility estimates over different time horizons?

I. asset returns are independent and identically distributed (i.i.d.)

II. volatility is constant over time

III. no serial correlation in the forward projection of volatility

IV. negative serial correlations exist in the time series of returns

- A. I, II and III

- B. I and III

- C. I and II

- D. III and IV

Answer: A

Explanation:

Explanation

The square root of time rule can be used to convert, say a 1-day volatility to a 10-day volatility, by multiplying the known volatility number by the square root of time to get the volatility over a different time horizon.

However, there are key assumptions that underlie the application of this rule, and statements I to III correctly state those assumptions. If serial correlations (whether negative or positive) exist, then asset returns are not independent as they are affected by the prior day or prior period's returns, and we cannot use the square root of time rule. Therefore Choice 'd' is the correct answer.

In order to use the 'square root of time' rule, asset returns should be iid, volatility should stay constant (ie there should be no volatility clustering), and no serial correlations (ie the returns of one day should not be affected by the returns of the prior periods). Choice 'd' is the correct answer.

NEW QUESTION 59

Which of the following statements is true:

I. A high market beta implies a high degree of correlation with the market II. Correlation coefficient and covariance between assets have the same sign III. A correlation of zero indicates the absence of a linear relationship between the two assets IV. Unless assets are perfectly correlated, diversification always reduces portfolio risk.

- A. I

- B. II, III and IV

- C. I, II, III and IV

- D. I and II

Answer: B

Explanation:

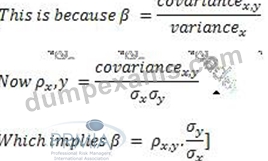

Explanation

A high beta does not necessarily imply a high correlation with the market. The relationship between beta and correlation can be expressed as 103.04.e2103.04.e2, where x is the market portfolio and y is

the asset under consideration.

103.04.e

This means that a high market beta could be due to high volatility of the asset in question, and not because of a high correlation. Therefore statement I is not correct.Statement II is correct as correlation and covariance have the same sign. This is because correlation = covariance/product of standard deviations. Since standard deviation is always positive, correlation and covariance will have the same sign.A correlation of zero indicates the absence of a linear relationship between two variables - therefore statement III is correct.Statement IV is correct as well, because unless correlation is +1, diversification always reduces total portfolio risk.

NEW QUESTION 60

The forward price of a physical asset is affected by:

- A. the spot price, the risk-free rate, carrying costs and any other cash flows from holding the asset

- B. The spot price of the asset and the market's prevailing view of the commodity's direction in the future

- C. the spot price, the risk-free rate, carrying costs, any other cash flows from holding the asset and the time to maturity of the forward contract

- D. the spot price, the risk-free rate, carrying costs, any other cash flows from holding the asset and the volatility of spot prices

Answer: C

Explanation:

Explanation

Choice 'b' lists all the factors that affect the forward price of a physical asset and is the most complete answer.

Forward prices for physical assets are not affected by volatility (only options are), nor are they arbitrarily decided by any prevailing 'views'.

NEW QUESTION 61

The most risky tranche of a structured credit derivative is called:

- A. the risky tranche

- B. the senior tranche

- C. the equity tranche

- D. the mezzanine tranche

Answer: C

Explanation:

Explanation

The riskiest tranche of a structured product is called the equity tranche. All other choices are incorrect.

NEW QUESTION 62

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.] Which of the following statements relating to convertible debt are true:

I. A hard call protection means the bond cannot be called by the issuer till the share price reaches a threshold II. It is advantageous for the issuer to call its convertible securities when the share price exceeds the conversion price III. When the issuer's share prices is very high, the convertible bond trades at a discount to the value of the shares it is convertible into IV. Convertible bonds generally have to carry a higher coupon than on equivalent non-convertible securities to make them attractive to investors

- A. I, III and IV

- B. II and III

- C. I and II

- D. III and IV

Answer: B

Explanation:

Explanation

A 'hard call protection' means the bond cannot be called until a certain date, regardless of what the share price is. Therefore statement I is false. Also note that a 'soft call protection' means that a bond can be called only if the share price reaches a certain threshold.

It is advantageous for the issuer to call its convertible securities when the share price exceeds the conversion price - because these shares can instead be sold in the market at the higher share price than the lower conversion price. Statement II is true.

When the issuer's share price is very high, the convertible bond trades at a discount to the share price because it is almost certain to be called by the issuer and be redeemed at par. Therefore statement III is right. Statement IV is incorrect because convertible bonds need to pay less coupon than equivalent non-convertible bonds because of the value of the option embedded in them.

NEW QUESTION 63

Which of the following statements are true for a portfolio of two assets:

I. Given volatility, weights and correlation, combined standard deviation cannot be calculated without additional information on covariances.

II. When the two assets are perfectly negatively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

III. When the two assets are uncorrelated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

IV. When the two assets are perfectly positively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

- A. II and IV

- B. IV

- C. All of the above

- D. I and III

Answer: B

Explanation:

Explanation

Given volatility, weights and correlation, we do not need any additional information on covariances - and therefore statement I is incorrect.

To evaluate the other statements, consider the formula for portfolio variance (recalling that standard deviation is just the square root of the variance) portfolio_var_diff_corr Statement II is incorrect because this statement describes what the standard deviation of the portfolio would be if the assets were to be perfectly positively correlated (here they are negatively correlated).

Statement III is incorrect. When the two assets are uncorrelated (ie correlation = 0), the combined standard deviation is the square root of the weighted sum of variances, where the squares of the asset weights are used as weights (see formula above).

Statement IV is correct. When the assets are perfectly positively correlated, they are effectively the same asset and the combined standard deviation of a portfolio of such assets is nothing but the sum of their weighted standard deviations.

Also refer to the tutorial (and the Excel model - you will find it under Exam 2) for portfolio variances to see how portfolio volatility behaves when correlations are -1, 0 or +1.

NEW QUESTION 64

Calculate the settlement amount for a buyer of a 3 x 6 FRA with a notional of $1m and contract rate of 5%.

Assume settlement rate is 6%.

- A. Receive $2463

- B. Pay $9434

- C. Receive $9434

- D. Pay $2463

Answer: A

Explanation:

Explanation

An m x n FRA is an agreement to borrow money for a period starting at time m and ending at time n at the contracted rate. Therefore, the buyer of the 3 x 6 FRA has committed to borrow $1m at the beginning of 3 months and return it at the end of 6 months, ie a total borrowing period of 3 months at a rate of 5%. Of course, the $1m is never actually exchanged, and at the beginning of the 3 month period when the next three months' interest rate is known (6%), the parties merely exchange the difference in the interest. SInce this interest was only due at the end of the 6 months and is being exchanged at the 3 month time point, it will have to be discounted to its present value.

The correct answer to this question is =(1,000,000 * (6% - 5%) * 3/12)/(1 + (6%*3/12))=$2463.05. Since interest rates rose, the borrower gained as he has the right to borrow at a lower rate, and therefore the seller will pay the borrower.

(Here:

- $1m is the notional

- 6% - 5% represents the difference between the contracted and the realized interest rates

- 3/12 is the 3 month period from month 3 to 6

- Finally, we divide by the current interest rate for 3 months to present value the payment from month 6 to month 3)

NEW QUESTION 65

Which of the following will have a higher reinvestment risk when compared to a 6% bond issued at par?

Assume all bonds have identical yield to maturity.

I. A coupon bearing bond with a coupon rate of 2%

II. An amortizing bond

III. A coupon bearing bond with a coupon rate of 11%

IV. A zero coupon bond

- A. II and III

- B. I and III

- C. I, II and IV

- D. II, III and IV

Answer: A

Explanation:

Explanation

Imagine a bond that provides just two cash flows: $100 in one year and $10 in 10 years. Imagine another bond that pays nothing now but $100 in 10 years. Assume that both have identical yields to maturity. Yet despite the identical YTM, the bonds are quite dissimilar. For the first bond, we face the risk that we would receive the bulk of the present value of the bond in an year's time, and while there is a small amount due in 10 years, the first payment may not find an equally attractive investment opportunity. Reinvestment risk refers to the risk that cash flows from a bond may not be investible at the yield to maturity for the bond. In such cases, bonds that have longer durations are preferable.

A coupon bearing bond with a coupon rate lower than our benchmark bond will carry a lower reinvestment risk as its cash flows are weighted more towards the end. An amortizing bond returns a part of the principle periodically, increasing reinvestment risk. A higher coupon bearing bond will have a higher reinvestment risk, and a zero coupon bond will have the least reinvestment risk.

NEW QUESTION 66

A bond pays semi-annual coupons at an annual rate of 10%, and will mature in a year. What is its modified duration? Assume the yield curve is flat for the next 12 months at 5%.

- A. 0.953

- B. 0.700

- C. 1.500

- D. 1.000

Answer: A

Explanation:

Explanation

We can calculate the duration of the bond as follows:

PV of 1st coupon payment: $5/(1 + 5%/2) = $4.878

PV of final payment: $105/(1 + 5%) = $100

Weighted average of the two = (0.5*$4.878 + 1*$100)/($4.878 + $100) = 0.9767, ie this is the Macaulay duration.

Thus the modified duration is 0.9767/(1 + 5%/2) = 0.9529

(Note that Modified Duration = Macaulay Duration/(1 + y/n), where n is the compounding frequency) In addition to this calculation, in this particular question we can intuitively arrive at the correct answer by eliminating the incorrect choices. Since the bond matures in a year, its modified duration will be less than a year. Therefore Choice 'a' and Choice 'b' cannot be correct. Similarly, 0.700 appears too low as the coupons are not so heavily weighted towards earlier in the year. Therefore only Choice 'c' can be the correct answer.

NEW QUESTION 67

A trader finds that a stock index is trading at 1000, and a six month futures contract on the same index is available at 1020. The risk free rate is 2% per annum, and the dividend rate is 1% per annum. What should the trader do?

- A. Buy the index spot and sell the futures contract

- B. Buy the index spot and buy the futures contract

- C. Buy the futures contract and sell the index spot

- D. Sell the futures contract

Answer: A

Explanation:

Explanation

The fair price for the futures contract should be [1000 x ( 1 + (2%-1%)/2)] = 1005. This means the futures contract is 'rich' at 1020. The trader should therefore short the futures contract, and buy the index spot. To buy the spot index, he will incur a borrowing cost of 2%, which will be partly offset by the dividend yield of 1%, and at the end of six months he will owe a net amount of 1005 and hold the index. At the same time the futures contract would expire too, and he would be able to sell at the agreed price of 1020, making a risk free profit of

15.

NEW QUESTION 68

A zero coupon bond matures in 5 years and is yielding 5%. What is its modified duration?

- A. 4.76

- B. 5.25

- C. 0

- D. 1

Answer: A

Explanation:

Explanation

A zero coupon bond has a Macaulay duration equal to its maturity, ie in this case 5 years. We can calculate modified duration from Macaulay duration by using the following relationship:

Modified duration = Macaulay duration/(1 + y) where y is the yield.

Therefore the correct answer is 5 / (1.05) = 4.76.

Or intuitively, all the other answers appear clearly incorrect: 5 and 5.25 are too high, and 4 is too low.

Therefore the only reasonable choice is 4.76.

NEW QUESTION 69

A futures contract is quoted at 105. Which is the cheapest-to-deliver bond for this contract if there are three available bonds, quoted at 97, 101 and 106 with conversion factors respectively of 0.9, 1 and 1.1 respectively?

- A. The bond quoted at 97

- B. The bond quoted at 101

- C. The bond quoted at 106

- D. All the bonds are equally cheap to deliver

Answer: C

Explanation:

Explanation

Treasury bond futures do not specify which bond can be used to effect delivery, but allow the seller to pick from a number of available bonds. As a result, one of these eligible bonds emerges as being the 'cheapest' to deliver, and this CTD bond is determined by the basis between the cash price of the bond and the futures spot price as adjusted by the conversion factor for this specific bond. (ie, basis = Cash Price of the Bond - (Futures Price x Conversion Factor).) The bond with the lowest basis is generally the CTD. In the given question, the three basis calculations are:

1) 97 - (0.9 x 105) = 2.5

2) 101 - (1 x 105) = -4

3) 106 - (1.1 x 105) = -9.5

Since the third bond with a quote of 106 has the lowest basis, Choice 'b' is the correct answer.

NEW QUESTION 70

A company has a long term loan from a bank at a fixed rate of interest. It expects interest rates to go down.

Which of the following instruments can the company use to convert its fixed rate liability to a floating rate liability?

- A. A fixed for floating interest rate swap

- B. A currency swap

- C. Interest rate futures

- D. A forward rate agreement

Answer: A

Explanation:

Explanation

A fixed for floating interest rate swap would be the most appropriate to the company's needs. It will allow it to receive a fixed rate (which will offset the fixed payment it has to make on the loan) and pay a floating rate which it expects will be lower than the fixed rates. Choice 'a' is the correct answer.

NEW QUESTION 71

Which of the following is true about the early exercise of an American call option:

- A. An early exercise of an American call option is never a good idea as an option is always worth more alive than when it is dead

- B. An early exercise of an American call option is advisable whenever the option is deep in the money and delta approaches 1

- C. An early exercise of an American option, if ever to be done, should be done immediately after an ex-dividend date

- D. An early exercise of an American call option may be justified if an extraordinarily large dividend payment is imminent

Answer: D

Explanation:

Explanation

Generally, it is not a good idea to exercise an option early as any more upside in the remaining period to expiry is being sacrificed. However, if an extraordinarily large dividend is coming due, and this dividend is larger than the interest foregone from holding the option, it may be a good idea to exercise the option early. In such cases, the exercise needs to happen before the ex-dividend date and not afterwards. Choice 'b' is therefore the correct answer.

Even if the option is deep in the money and delta is approaching 1, and exercise upon maturity is almost a certainty, it would still always be better to sell the option than exercise it . Therefore Choice 'a' is incorrect.

Choice 'c' is correct in all cases except when a large dividend is coming in. Choice 'd' is not correct because an early exercise needs to happen prior to the ex-dividend date and not afterwards.

NEW QUESTION 72

Which of the following is NOT a historical event which serves as an example of a short squeeze that happened in the markets?

- A. The great silver squeeze, 1979-80

- B. The great Chicago fire, 1872

- C. The wheat squeeze, 1866

- D. The CDO squeeze, 2008

Answer: D

Explanation:

Explanation

There was no event such as the CDO squeeze in 2008. (Quite on the contrary, securitized products were selling at distressed prices.).

The silver squeeze of 1979-80 (Hunt brothers), the Chicago fire of 1872 (leading to a short squeeze on wheat), and the wheat squeeze (Hutchingson) of 1866 are real historical events that led to short squeezes in commodity markets. Choice 'b' is therefore the correct answer.

For the PRM exam, you should try to remember the event broadly, and the commodity involved.

NEW QUESTION 73

The rate of dividend on a stock goes up. What is the effect on the price of a put option on this stock?

- A. It may affect the put value either way depending upon the risk-free rate

- B. It increases the value of the put

- C. It does not affect the value of the put

- D. It decreases the value of the put

Answer: B

Explanation:

Explanation

Everything else remaining the same, an increase in the rate of dividends causes the value of call options to fall and the value of put options to rise. Therefore, Choice 'b' is the correct answer. (In the exam, the question could address either a call or a put option, so be aware of the answer in either case).

To understand this, consider how dividends are accounted for when valuing an option using the Black Scholes model. Future dividends are discounted to the present using the risk free rate and this discounted value is reduced from the spot price used in the BSM valuation. Effectively, this reduces the spot price used in the BSM formula. When the spot price reduces, and the exercise price remains the same, then the value of the call option goes down. In the same way, when spot price is reduced by the present value of dividends (and the exercise price stays the same), obviously the put option becomes more valuable. Therefore an increase in the rate of dividends increases the value of the put option.

There is another intuitive way to think about this: A call option is like a long position in the stock, but the holder of the call option is not entitled to receive dividends (unlike the holder of the stock). Since the holder of the call option has to forego the dividends, he is willing to pay less for the option; or in other words, the value of the call reduces.

In the same way, a put option is like having a short position in the stock. The holder of the short position has to borrow the stock in order to get into the short position in the first place. When dividends are paid, the holder of the short stock position has to make good any dividends that might be paid to the lender of the stock. The holder of a put option does not have to make any such payments. Therefore the put option is more valuable, and the existence of dividends (or an increase in dividends) increases the value of the put option.

(Try this out using the Black Scholes Excel model given under the tutorials by varying the spot price.)

NEW QUESTION 74

Which of the following portfolios would require rebalancing for delta hedging at a greater frequency in order to maintain delta neutrality?

- A. A portfolio with a low gamma

- B. A portfolio with a high delta and low gamma

- C. A portfolio with a high gamma

- D. A portfolio with a low delta and high vega

Answer: C

Explanation:

Explanation

A portfolio loses its delta neutrality if the delta of the portfolio changes but the underlying hedge is unchanged.

The portfolio that will require the most rebalancing will be one whose delta changes by larger amounts in response to a given change in the price of the underlying. The sensitivity of the changes in delta in response to changes in the price of the underlying is measured by gamma. The higher the gamma, the more the portfolio will go out of delta neutrality given a change in the price of the underlying. Therefore Choice 'b' is the correct answer.

A portfolio with a low gamma will maintain its delta over a larger price range for the underlying, and is therefore likely to require less frequent rebalancing. The absolute level of the delta itself does not matter, what matters is the gamma. Vega is irrelevant to the delta hedging decision. Therefore the other choices are incorrect.

NEW QUESTION 75

If x represents wealth, and u(x) its utility, then a logarithmic utility function can be represented by:

- A. u(x) = ln(x)

- B. u(x) = ln(-x)

- C. u(x) = 1/ln(x)

- D. u(x) = exp(x)

Answer: A

Explanation:

Explanation

A utility function provides a description of an individual or a firm's risk attitude. It expresses how risk seeking or risk averse they are. The utility function would provide for changes between risk seeking and risk averse behavior, for example, as an individual becomes richer, he may seek (or shun) risk more than before. A utility function incorporates all of this, and a logarithmic utility function is represented by u(x) = ln(x).

NEW QUESTION 76

A bank sells an interest rate swap to its client, with the client agreeing to pay the bank a fixed 4% and receive

3 month LIBOR + 100 basis points, payments due every quarter. After quarter 1, the 3 month LIBOR is 2% pa. Which of the following payments will happen in respect of this swap, assuming the contract notional is

$100m, and the rate convention is 30/360.

- A. Bank pays customer $1,000,000

- B. Bank pays customer $250,000

- C. Bank pays customer $1,000,000 and customer pays the bank $750,000

- D. Customer pays bank $250,000

Answer: D

Explanation:

Explanation

In an interest rate swap, only the net payment is made. In this case,

- the customer pays the bank 4%*(3/12)*$100m

- the bank owes the customer (2% + 100bp))*(3/12)*$100m

Therefore the customer pays (4% - (2% + 100bp))*(3/12)*$100m. 3/12 represents the 3 month time interval.

This is equal to a net payment of $250k from the customer to the bank. Therefore Choice 'c' is the correct answer and the rest are incorrect.

NEW QUESTION 77

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.] A company that uses physical commodities as an input into its manufacturing process wishes to use options to hedge against a rise in its raw material costs. Which of the following options would be the most cost effective to use?

- A. Writer-extendible options

- B. Vanilla options

- C. Correlation options

- D. Average rate options

Answer: D

Explanation:

Explanation

Average rate options will be the most cost effective in this scenario as they are cheaper than vanilla options.

Writer extendible options on commodities will be even more expensive, and correlation products are irrelevant to the manufacturing company's hedging needs.

NEW QUESTION 78

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.] Which of the following best describes a shout option

- A. an option in which the buyer of the option has the option to extend the expiry of the option upon the payment of an extra premium

- B. an option in which the holder of the option has the right to reset the strike price to be at-the-money once during the life of the option

- C. an option whose expiry is automatically extended if it finishes out of the money.

- D. an option which kicks in as a plain vanilla option if the underlying hits an agreed threshold

Answer: B

Explanation:

Explanation

Choice 'c' correctly describes a 'holder extendible option'. Choice 'd' describes a 'writer extendible option'.

Choice 'a' describes a 'shout option'. Choice 'b' describes a 'knock in' option.

NEW QUESTION 79

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the 2 year swap rate is 5%, and the yield curve is also flat at 5%

- A. $1,859,410

- B. -$1,859,410

- C. $1,904,762

- D. -$1,904,762

Answer: A

Explanation:

Explanation

The swap can be valued by using the new swap rate of 5%. The investor is paying fixed and receiving LIBOR, and can effectively get out of his position by entering into a swap to receive 5% and pay LIBOR. This will leave him/her with a net cash flow of 1% for two years, ie $1m for 2 years that can be discounted to the present using the rates provided, ie =(1/1.05 + 1/(1.05^2)) = $1,859,410.

Detailed explanation:

An Interest Rate Swap exchanges fixed interest flows for floating rate flows. The floating rate leg is tied to some reference rate, such as LIBOR. The parties exchange net cash flows periodically. Conceptually, an interest rate swap is the combination of a fixed coupon bond and a floating rate note. The party receiving the fixed rate is long the fixed coupon bond and short the FRN, and the party receiving the floating rate is long the FRN and short the fixed coupon bond.

An interest rate swap can be valued as the difference between the two hypothetical bonds. FRNs sell for par at issue time as they pay whatever the current rate is, subject to periodic resets. Therefore immediately after a payment is made on a swap, the value of the FRN component is equal to its par value. The bond can be valued by discounting its cash flows. The difference between the two represents the value of the swap. When the swap is entered into, the fixed rate leg is set in such a way that the value of the hypothetical bond is equal to that of the FRN, and the swap is valued at zero. The rate at which the fixed rate leg is set is called the swap rate. Over its life, market rates change and the value of the fixed coupon bond equivalent in our swap diverges from par (whereas the FRN stays at par - at least right after payments are exchanged and the new floating rate is set for the next period). Thus the swap acquires a non-zero value.

There are two ways to value a swap. If interest rates for the future are known, the bond and the FRN can be valued and their difference will be equal to the value of the swap. Sometimes, the current swap rates are known. In such a case, the swap can be valued by imagining entering into an opposite swap at the new swap rate, which will leave a residual fixed cash flow for the remaining life of the swap. This residual cash flow can be valued and that represents the value of the swap. For example, if a 4 year swap was entered into exchanging an annual fixed 5% payment on a notional of $100m for a floating payment equal to LIBOR, and at the end of year 1 the swap rate is 6%, then the party paying fixed can choose to enter into a new swap to receive 6% and pay LIBOR. All cash flows between the old and the new swap will offset each other except a net receipt of 1% for the next 3 years. This cash flow can be valued using the current yield curve and represents the value of the swap.

NEW QUESTION 80

If x is the standard deviation of the asset to be hedged, and y is the standard deviation of the asset being used to hedge against price movements in x, then the minimum variance hedge ratio is given by which of the following expressions (given that x,y is their correlation) A)

B)

C)

D)

- A. Option A

- B. Option D

- C. Option B

- D. Option C

Answer: B

Explanation:

Explanation

The minimum variance hedge ratio answers the question of how much of the hedge to buy to hedge a given position. It minimizes the combined volatility of the primary and the hedge position. The minimum variance hedge ratio is given by the expression 103.10.b103.10.b. Effectively, this is the same as the beta of the primary

position with respect to the hedge.

All other choices are incorrect.

Intuitive understanding of the hedge ratio: There are two standard deviations in play here: one, the standard deviation of the asset to be hedged (x), and two, the standard deviation of the asset being used as the hedge(y).

Now assume an extreme case where both the asset to be hedged and the asset being used as the hedge have a correlation of 1. (That keeps the calculation simple.). Also assume that the std dev of the asset to be hedged is

10% annually, and that of the asset being used as a hedge is say 20%. At this point, just ignore all formulae, and think intuitively about how much of the hedge should we buy to have the same risk (in the opposite direction) as the primary position but in the opposite direction so the variation in the primary position is cancelled by opposite movements in the hedge position. Obviously, we need to buy half because the asset being used as a hedge is twice as volatile. In other words, we divided the volatility (std dev) of the primary position by the volatility of the asset being used as a hedge.In this question, x is the standard deviation of the asset to be hedged, and y is the standard deviation of the asset being used to hedge. We will need to divide x by y.

NEW QUESTION 81

......

PRM Free Certification Exam Material from Dumpexams with 290 Questions: https://www.dumpexams.com/8006-real-answers.html